Series T mutual funds offer a smart, tax-efficient way to generate steady cash flow from your investments, especially in retirement.

Key messages:

- Predictable cash flow: Series T mutual funds aim to provide consistent monthly distributions that can help cover your cash flow needs.

- Tax efficiency: Series T distributions often include return of capital, which is generally more tax efficient than other forms of income.

- Stay invested: As cash flow needs change, investors can transition from Series A to Series T of the same fund without triggering a taxable event, helping convert savings into cash flow while remaining invested.

When the time comes to shift your investment strategy from saving to spending, you want cash flow that’s consistent, predictable and tax efficient. That’s where Series T mutual funds can help.

What is Series T?

Series T mutual funds are suitable for investment in non-registered accounts and can provide regular monthly distributions based on an annual target rate, such as 3%, 4%, or 5%. While the actual distribution amounts may vary, you’ll have a good idea of how much cash flow you can expect from your investment each month based on the fund’s target distribution rate.

Who should consider Series T?

- Those investing inside non-registered accounts

- Investors looking for steady, tax-efficient cash flow

- People transitioning into retirement, already retired, or investors looking to supplement other income sources

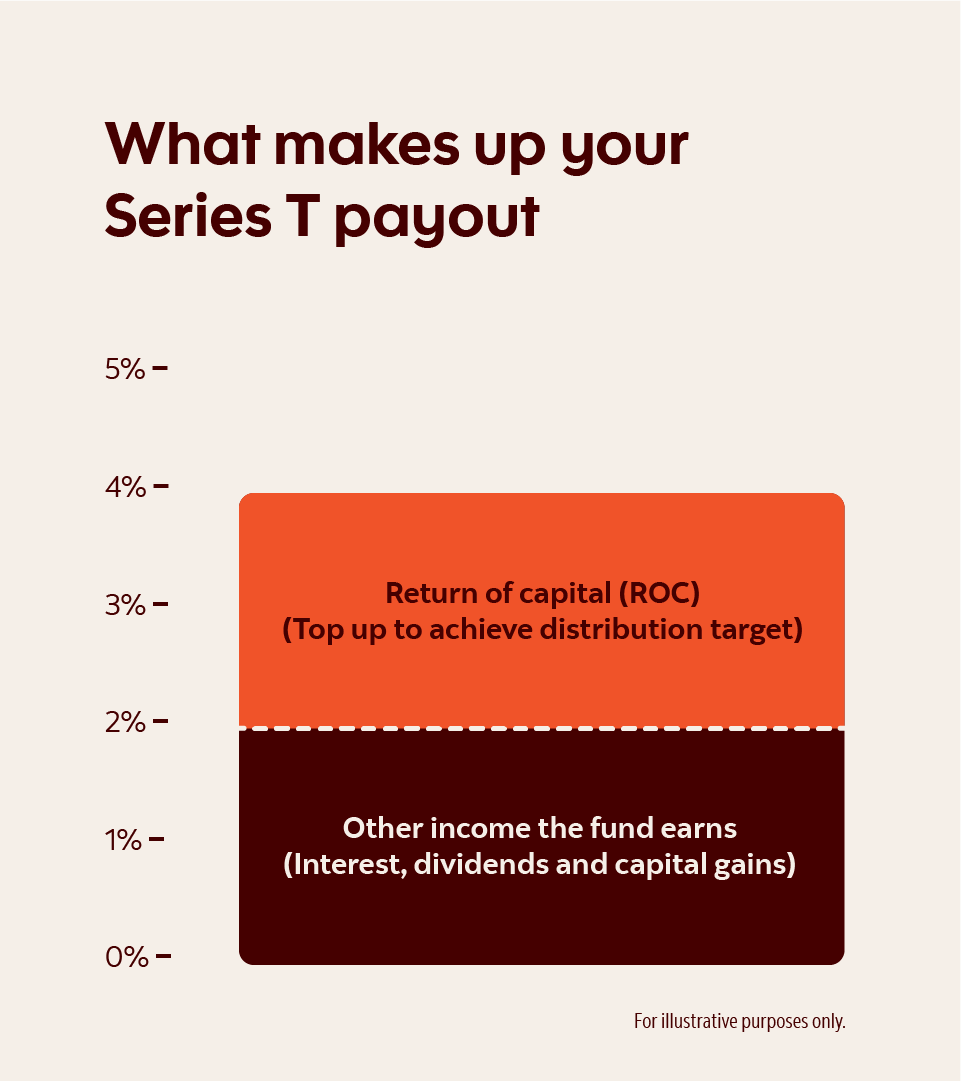

What’s in a Series T distribution?

When it comes to cash flow, it’s not just about how much your investments earn—it’s about how much you keep after tax. That’s where Series T can help. Series T mutual funds provide a fixed monthly amount of cash flow that may consist of:

- Interest, dividends, and realized capital gains earned by the fund (i.e., the fund’s income), and/or

- Return of Capital (“ROC”), which is a portion of your original investment.

How ROC works

ROC may be used to supplement the target Series T payout when the fund’s income isn’t enough on its own:

- If the fund’s income is less than the Series T fixed payout amount, ROC is used to top up the distributions.

- If the fund’s income is equal to or greater than the Series T fixed payout amount, no ROC is needed.

- Conversely, if the fund does not have any income to distribute, the Series T payment may be made entirely of ROC.

In the hypothetical example shown with a 4% fixed target payout, the fund’s income of 2% is less than the fixed target, and ROC fills in the gap to reach the target amount.

Tax considerations

ROC is generally not immediately taxable when received. Instead, it reduces your adjusted cost base (ACB). When you eventually sell your investment, a lower ACB may result in a higher capital gain or a smaller capital loss. When the ACB reaches zero, any subsequent ROC distributions will be taxable as a capital gain in the year it’s received.

Stay invested while receiving income

Series T funds aim to pay a regular distribution that may consist of ROC and other income sources generated by the fund without requiring you to sell your investments.

Unlike redeeming your mutual funds or using an automatic withdrawal plan (AWP)—which can trigger capital gains or losses—Series T provides cash flow without having to sell your investments, making it generally more tax efficient.

This hypothetical example illustrates investing $100,000 in a Series T mutual fund with an annual distribution of 4%, half of which consists of ROC. With an assumed annual growth rate of 6%, over a 25-year period, the investment grows to over $160,000 (solid line), while paying more than $128,000 in cumulative pre-tax cash flow (bars). As indicated by the dotted line, the ROC portion of the cash flow reduces the adjusted cost base, as the initial investment of $100,000 is slowly returned.

Series T funds offer steady, tax‑efficient cash flow, including ROC distributions that can defer taxes until the sale of your investment or when the ACB reaches zero (i.e., the initial investment is fully returned), all while maintaining the potential for investment growth.

Plan your cash flow and find the right investment for you

Cash flow planning involves more than just receiving payments. It also includes managing taxes and choosing investments that match your goals. As part of your personal cash flow strategy, we can help recommend an approach that works for you.

For example, if you already own a Series A of a Scotia Portfolio Solution in your non-registered account, you can switch to Series T of the same fund—also known as a reclassification—without tax implications. This conversion may be particularly beneficial when transitioning from saving to spending, like when you enter retirement.

ScotiaFunds offers Series T options with annual payout rates of 3%, 4%, or 5% in a variety of portfolio options to suit your unique investing preferences. To learn more about investment solutions that can meet your income needs, try using the Series T cash flow calculator.

This publication is provided for information purposes only. It is not to be relied upon as financial, tax or investment advice or guarantees about the future, nor should it be considered a recommendation to buy or sell. Information contained in this document, including information relating to interest rates, market conditions, tax rules, and other investment factors, are subject to change without notice, and The Bank of Nova Scotia is not responsible to update this information. All third-party sources are believed to be accurate and reliable as of the date of publication, and The Bank of Nova Scotia does not guarantee its accuracy or reliability. Readers should consult their own professional advisor for specific financial, investment and/or tax advice tailored to their needs to ensure that individual circumstances are considered properly, and action is taken based on the latest available information. This publication may contain forward-looking statements based on current expectations and projections about future general economic factors. Forward-looking statements are subject to inherent risks and uncertainties which may be unforeseeable and such expectations and projections may be incorrect in the future. Forward-looking statements are not guarantees of future performance and you should avoid placing undue reliance upon them. This publication and all the information, opinions and conclusions contained herein are protected by copyright. This publication may not be reproduced in whole or in part without the prior express consent of The Bank of Nova Scotia.

Commissions, trailing commissions, management fees and expenses may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed or insured by the Canada Deposit Insurance Corporation or any other government deposit insurer; their values change frequently, and past performance may not be repeated.

Investors holding funds in a non-registered account should be aware that distributions are taxable. The amount and the tax characteristics of distributions made to non-registered accounts will be reported on tax slips that will be sent to investors. Distributions made to registered accounts such as an RSP or RIF are not taxable.

Target distributions are not guaranteed and may change at any time at the discretion of the fund’s Manager. If distributions paid by the fund are greater than the net income and net capital gains of the fund, distributions paid may include a return of capital. A return of capital is not taxable to the investor but will generally reduce the adjusted cost base of the securities held for tax purposes. If the adjusted cost base falls below zero, investors will realize capital gains equal to the amount below zero. Distributions are automatically reinvested unless an investor elects to receive them in cash. Investors should not confuse a fund’s distribution rate with its performance, rate of return or yield. Distributions may consist of net income, and/or dividends, and/or net realized capital gains and are taxable in the hands of the investor. Target monthly distributions are determined based on the target payout rate for the indicated series of the fund. Monthly distributions are made by the last business day of each month, or the last business day of each calendar quarter for quarterly paying fund series, other than in December. The final distribution in respect of each taxation year will be paid or payable by December 31 of each year or at such other times as may be determined by the fund’s Manager.

ScotiaFunds® are managed by Scotia Global Asset Management. ScotiaFunds are available through Scotia Securities Inc. and from other dealers and advisors. Scotia Securities Inc. is wholly owned by The Bank of Nova Scotia and is a member of the Canadian Investment Regulatory Organization.

Scotia Global Asset Management is a business name used by 1832 Asset Management L.P., a limited partnership, the general partner of which is wholly owned by Scotiabank.

Scotiabank® includes The Bank of Nova Scotia and its subsidiaries and affiliates, including 1832 Asset Management L.P. and Scotia Securities Inc.

® Registered trademarks of The Bank of Nova Scotia, used under licence.

© Copyright 2026 The Bank of Nova Scotia. All rights reserved.