If you’ve ever looked at a bill and appreciated seeing the total cost you paid, you already understand the idea behind Total Cost Reporting (TCR). Starting in early 2027, TCR applies the same idea to investing by providing greater transparency into total investment costs. This article offers a plain‑language overview of what TCR means for you and your investments.

What is Total Cost Reporting?

Total Cost Reporting (TCR for short) is a Canadian regulatory initiative meant to give investors like you a more complete picture of what it costs to own an investment fund — including costs built into investment funds like mutual funds and Exchange Traded Funds (ETFs).

The goal is simple: Make investment costs clearer, so understanding them is easier. That way, Canadians can make more informed investment decisions.

How did we get here?

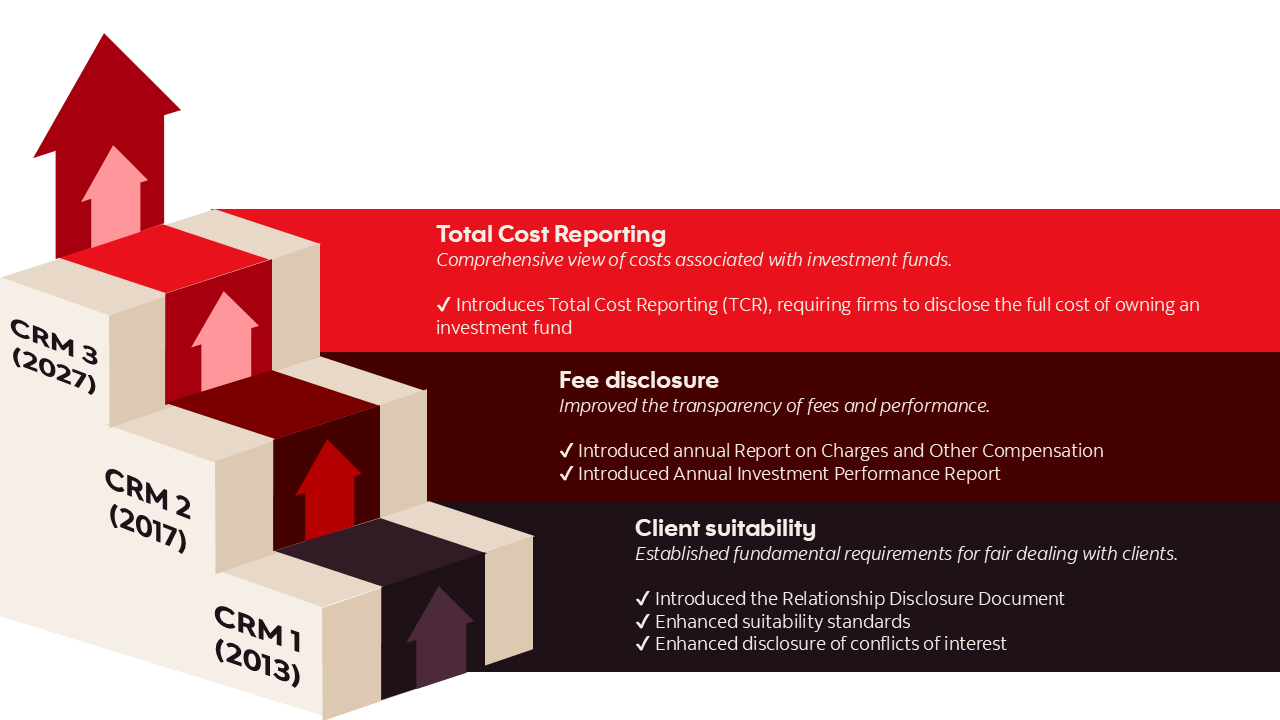

TCR represents the third and latest phase of Canada's Client Relationship Model (CRM) — a set of reforms which began in 2013, designed to enhance transparency and protection for investors (see Figure 1).

Figure 1: Built over time, with investors in mind

Are these new fees?

No, these are not new or additional fees. The costs you'll see already exist—TCR simply makes them easier to see and understand.

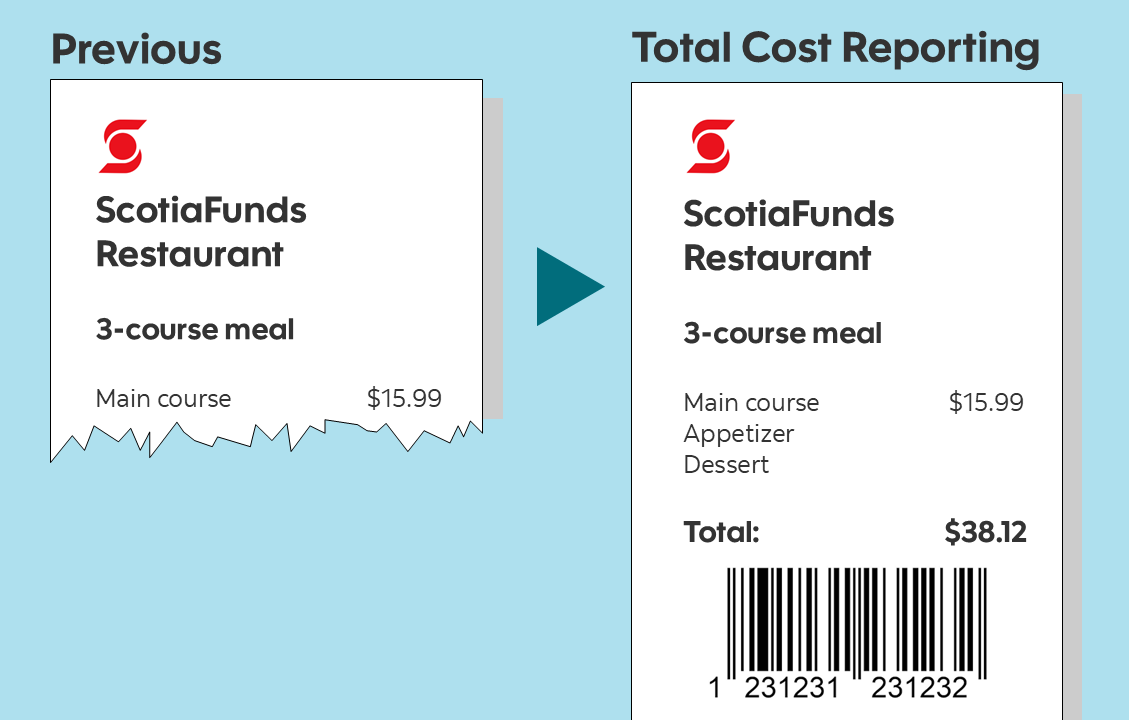

Think of it like a restaurant bill (see Figure 2). You order a three‑course meal and the total is $38.12 either way, but the bills you get are different:

- Bill 1: Main course = $15.99

- Bill 2: Total = $38.12

Which bill would you prefer receiving? The same 3-course meal, same total paid — but with Bill 2, you see the total cost, as opposed to just a part of it. That’s the guiding principle behind TCR.

Figure 2: TCR shows the full cost, not just part of it

What fees will I see — and what do they mean?

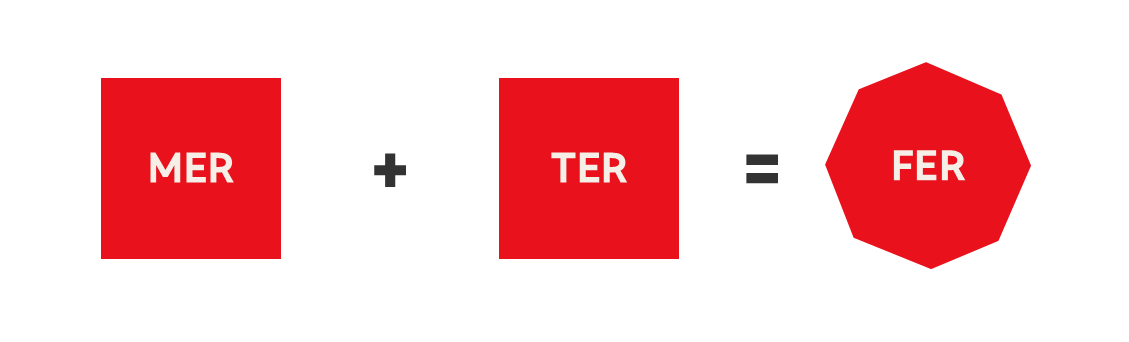

Total Cost Reporting doesn’t replace what you see today, it adds to it. You’ll continue to see charges and compensation already disclosed (like trailing commissions associated with advice and service, if you work with an advisor). In addition, you’ll now see the total embedded fund costs (see Figure 3) which are built into the fund and reflected in its returns, not billed to you separately. Here’s what they are in plain language:

Figure 3: The components of Total Cost Reporting

Management Expense Ratio (MER)

Think: M = Management.

The ongoing cost of owning a mutual fund that covers professional investment management, operating expenses, and taxes—and, in some fund series, advisor compensation. These underlying costs are embedded within the fund, meaning they are not charged separately to investors.

Trading Expense Ratio (TER)

Think: T = Trading.

Reflects the costs associated with buying and selling securities within the fund. These trading-related costs are embedded within the fund, rather than charged separately to investors.

Fund Expense Ratio (FER)

Think: F = Full.

A new reporting term, but not a new fee. It combines MER + TER into one figure, offering a full view of total embedded fund costs, hence “total cost reporting”.

Putting it in perspective

What’s helpful is that these embedded costs will be shown two ways: as a percentage for each fund you own (the Fund Expense Ratio), and as a single total dollar amount across all your holdings (the fund expenses). This makes it easier to connect the costs to what it means for your investments. Suppose you had $100,000 invested in a fund with an MER of 1.5% and a TER of 0.2% (see Figure 4):

Figure 4: What it looks like in real life

| In % terms | In $ terms | ||

|---|---|---|---|

| Management Expense Ratio (MER) | 1.5% | Management expenses | $1,500 |

| Trading Expense Ratio (TER) | 0.2% | Trading expenses | $200 |

| Fund Expense Ratio (FER) | 1.7% | Fund expenses | $1,700 |

In this example, the 1.7% (FER) and the client’s fund expenses of $1,700 will both appear on the annual fee disclosure report, representing the embedded fund costs paid in the previous calendar year.

Where can I review these fees?

You’ll automatically see these fees shown more clearly on your annual fee disclosure report within your Personal Portfolio statement from Scotiabank starting January 2027, covering the 2026 calendar year.

This report is sent once a year and will be delivered to you—either by mail or electronically—based on how you’ve elected to receive your account statements. It will be included with your year‑end account statement.

Moving forward, you’ll continue to receive your annual fee disclosure report each year, reflecting investment costs incurred during the previous calendar year.

Does TCR apply to all investments?

A quick note on scope: TCR applies to investment products that have embedded costs¹— meaning fees built into the fund itself. This includes mutual funds and ETFs, among other investment types. Examples of investment types that are excluded from TCR include individual stocks, bonds, and GICs.

It’s also helpful to know that TCR applies across the industry. If you are a Canadian investor, the same cost transparency rules apply if you own investments with embedded costs no matter where you hold them.

What do I get in return for paying fees?

Think back to our earlier 3-course meal at a restaurant example. When you pay for a meal, you’re not just paying for the ingredients—you’re paying for the time saved and overall experience. Someone else plans the menu, sources the ingredients, prepares the meal, and cleans up afterward. You sit down and enjoy.

When you invest in mutual funds, fund fees work in a similar way. Here’s the value you can receive in return for the fees you pay:

Professional investment management: Mutual funds are built and overseen by professional teams who set the investment approach and keep it aligned with its objectives. In actively managed funds, portfolio managers research markets, select investments, and manage risk, while index‑tracking funds follow a clearly defined, rules‑based strategy under professional oversight. That’s why Canadian investors continue to value having a professional manage their investments for them, with more than half of investors favoring this approach.²

Convenience and time savings: Investing in a mutual fund saves you time from having to be your own financial advisor, portfolio manager, risk analyst, trader and more, so you don’t have to manage everything yourself.

Financial advice and coaching: Just like in life, having a coach helps keep you on track. The same goes for your finances by working with an advisor.

| What investors say about their advisor2 | % who agree |

|---|---|

| "My primary advisor understands my specific needs and makes appropriate recommendations" | 81% |

| "My primary advisor keeps me on track to meet my goals" | 78% |

| "My primary advisor helps me avoid making mistakes when buying and selling investments" | 74% |

Peace of mind: Knowing professionals are managing your investments and an advisor is supporting your investment plan can help reduce stress and uncertainty. 4 in 5 Canadians say their primary advisor makes them feel confident about their financial situation.²

Tools and resources: You may also gain access to digital tools and resources—such as Scotia Smart Investor—to help you monitor progress towards your investment goals.

¹ Investment fund securities include all Canadian, and foreign mutual funds, exchange traded funds, scholarship plans and Segregated Fund contracts. Exclusions include labour-sponsored investment funds, prospectus exempt funds, newly established funds less than 12 months before the end of the period covered by the statements and continued exemptions for non-individual permitted clients.

² Source: Scotia Global Asset Management Investor Sentiment Survey (Fall 2025).

This material is provided for information and educational purposes only and is not intended to provide investment, financial, legal, accounting or tax advice. The information contained herein should not be relied upon as a basis for any investment decision. Investors should consult their own professional advisor regarding their individual circumstances before making any investment decisions.

Commissions, trailing commissions, management fees and expenses may be associated with mutual fund investments. Please read the fund’s simplified prospectus before investing. Mutual funds are not guaranteed or insured by the Canada Deposit Insurance Corporation or any other government deposit insurer, their values change frequently, and past performance may not be repeated.

ScotiaFunds® are managed by Scotia Global Asset Management. ScotiaFunds are available through Scotia Securities Inc. and from other dealers and advisors, including ScotiaMcLeod® and Scotia iTRADE®, which are divisions of Scotia Capital Inc. Scotia Securities Inc. and Scotia Capital Inc. are wholly owned by The Bank of Nova Scotia. Scotia Capital Inc. is a member of the Canadian Investor Protection Fund and the Canadian Investment Regulatory Organization.

Scotia Global Asset Management® is a business name used by 1832 Asset Management L.P., a limited partnership, the general partner of which is wholly owned by Scotiabank.

® Registered trademarks of The Bank of Nova Scotia, used under licence.

© Copyright 2026 The Bank of Nova Scotia. All rights reserved.