For decades, most investment portfolios have been built around a simple idea: combine the growth potential of stocks with the stability of bonds, and adjust the mix over time as your goals and risk tolerance change. That stock‑and‑bond foundation is still important, but the world around it has shifted.

The post‑2020 inflationary period has brought heightened market volatility. When this is combined with periods of higher stock–bond correlations, at precisely the wrong times, investors can see both assets declining together, weakening the diversification they rely on...

The alternatives opportunity

That’s why more and more investors and portfolio managers are turning to alternative investments, or “alts,” as part of a broader toolkit for building more resilient portfolios.

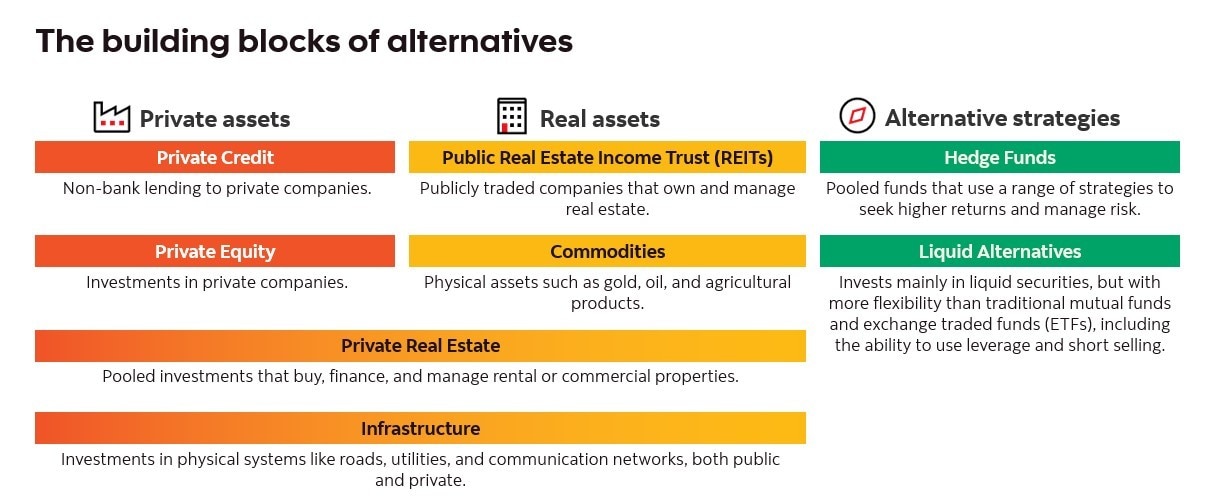

Figure 1: An overview of alternative investments

The case for alternatives isn’t just about innovation, it’s about responding to real shifts in how we live, work, and invest. Because, here’s the deal…

- Traditional 60/40 portfolios could be facing pressure. In volatile periods, stocks and bonds, especially higher‑yield bonds, have been more likely to drop together. This has reduced the protection investors usually expect from a 60/40 mix. We saw this in 2022. Bond yields started from very low levels, then inflation picked up and interest rates rose. That hurt both sides of the traditional portfolio: stock prices fell and bond values dropped as well, so investors experienced losses in both at the same time.

- Volatility is now the new normal and part of daily life. Public markets have become more volatile, so traditional portfolios may experience bigger ups and downs. Some investors may choose to take on more risk, but that approach doesn’t work for everyone and can lead to larger, harder‑to‑recover‑from drawdowns.

- Increased pressure on savings is reshaping financial plans. Higher living costs and longer lifespans mean people may need to save more just to maintain the same standard of living. And with fewer employer pensions available, more of the long‑term retirement burden now falls on individuals and families.

And so, investors are turning to alternatives because of what they add to their portfolio…

- A broader opportunity set. Alternative assets and strategies open the door to markets that are bigger, broader, and often less crowded than traditional public markets. As of recent estimates, only about 50 thousand companies trade on public exchanges worldwide, compared with well over 60 million that remain privately held.

- Stronger diversification and less correlation. Because alternative assets often move differently than stocks and bonds, they can help ensure your whole portfolio isn’t dragged down all at once in a downturn, smoothing returns and reducing volatility.

- Enhancing your return potential. Liquid alternative strategies are more flexible and can use a wider toolkit than traditional mutual funds, such as leverage, derivatives, and long/short approaches, which could offer greater return potential than a traditional stock‑and‑bond portfolio.

With alternatives, the goal isn’t to replace your core investments, it’s to complement them. They add more tools to help support your long‑term plan by aiming to improve your portfolio’s overall risk‑adjusted returns.

But there’s a catch…

Alternatives are complicated and can be complex to access and manage.

Access

Many alternative asset classes are designed for large institutions or high‑net‑worth investors, with high minimum investments, long lockup periods, limited liquidity, and added structural complexity that can be challenging for individual investors.

Management

Building and maintaining an alternatives allocation requires specialized research and due diligence, detailed legal and tax work, and often less frequent reporting from underlying investments, all within more complex governance and risk frameworks.

And so, while alternatives can add meaningful value to a portfolio, they typically demand significant access, expertise, and infrastructure to include in a portfolio effectively.

An alternative way to add alts to your portfolio

So, what’s the easiest way to access alternatives? That’s where Scotia INNOVA Portfolios come in, this program takes the complexity out of investing in alternatives. With INNOVA, you access alternatives through a mutual fund structure for a minimum investment of $500 or a pre‑authorized contribution of just $25 a month, making it a straightforward way to bring them into your portfolio.

1 in 6 Canadian investors already use alternatives, and that number is growing as more people see their potential.

Each Scotia INNOVA Portfolio:

Starts with a disciplined, long‑term mix of equities and fixed income that is calibrated to a specific risk profile, so your core allocation stays aligned with your goals and comfort with risk.

Adds complementary alternative asset classes and strategies, such as private assets and liquid alternatives, to deepen diversification and build resilience.

Is managed by Scotia’s Multi‑Asset Management Team using research‑driven strategic and tactical asset allocation that incorporates both traditional assets and alternatives.

With INNOVA, you benefit from alternative thinking, better diversification, more robust risk management, and new sources of potential return. Your allocation to alternatives sits inside a complete, professionally managed portfolio that adapts as markets and your needs evolve, bringing traditional and alternative investments together into one resilient solution to support your goals.

See the Multi-Asset Management Team’s current views on alternatives