When you hear “active vs passive,” it can sound like you have to pick a side… In reality, most investors don’t stay in one camp forever; they often use a mix of approaches over time (or even at the same time), depending on their goals, time horizon, and comfort with risk.

In this article, we focus on how active and passive management strategies work within equity portfolios, where both approaches are widely used. Because understanding what each style can (and can’t) do for you is the first step to putting them to work in a thoughtful way.

What do we mean by “active” and “passive?”

Active strategies use professional portfolio managers and research teams to decide what to own, how much to own, and when to make changes to those holdings. The goal is to do better than a benchmark (which is often an index like the S&P 500 or the S&P/TSX Composite) over time, after fees, and while managing risk. That can mean:

- Investing in companies with stronger fundamentals, growth prospects, or more attractive valuations

- Adjusting region, sector, or security weights as conditions change

Passive strategies are designed to track a specific index. There is no independent research, stock‑by‑stock selection, or valuation work; when the index changes, the fund simply adjusts to mirror it. The goal is to match the market, before fees, not to beat it.

Both approaches can play a useful role. The key is deciding where each one fits in your portfolio.

Mutual funds vs Exchange-Traded Funds (ETFs): clearing up common misconceptions

Because “active vs passive” often gets mixed up with “mutual funds vs ETFs,” it can be helpful to separate the two.

- You can have active mutual funds (most common) and passive mutual funds (index funds)

- You can also have passive ETFs (most common) and actively managed ETFs

In other words, the fund structure (mutual fund or ETF) doesn’t tell you by itself whether the strategy is active or passive.

Where active management can add value

Traditional index or passive mutual funds/ETFs often shine in strong, momentum‑driven bull markets, when simply owning the market does most of the work. But when markets are uneven across regions, sectors, or companies, active management can add value—especially in downturns—by tilting toward more resilient areas and using tools to manage risk.

Did you know?

Just 10 companies make up ~35% of the S&P 500.

Beyond that, active managers outperform by:

- Avoiding the most crowded parts of an index, especially when a few mega‑cap names dominate returns

- Looking for opportunities in areas the index doesn’t fully cover

- Aiming for return patterns that don’t move in lockstep with the benchmark, to help diversify your overall portfolio

None of this eliminates risk, or guarantees outperformance every year, but it highlights how active management can help navigate more complex markets.

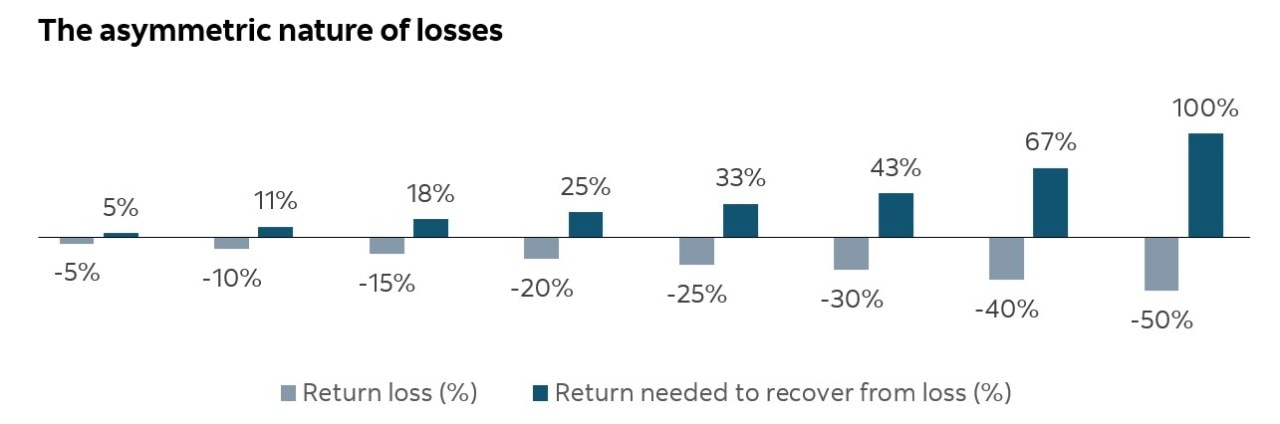

One of the reasons active risk management matters so much is that losses are asymmetrical. A 10% decline only needs an 11% gain to get back to even, but a 50% decline requires a 100% return just to recover. You can see here how quickly the required return climbs as losses deepen, and why active strategies that aim to cushion larger drawdowns can play an important role in a long-term plan.

Where passive management shines

All that said, passive strategies bring their own advantages, particularly around cost and simplicity.

- Efficient and easy access to broad markets

- Clear rules for what the fund owns and why, as it simply tracks the index, no more and no less

- Lower headline fees for index‑tracking mutual funds and ETFs

For many investors, passive funds are a straightforward way to build a diversified core, especially in very liquid, well‑researched markets where it’s harder for active managers to stand out consistently.

A word about fees: why it’s not always an apples-to-apples comparison

Fees matter; they come directly out of your returns over time, but comparing them can be more nuanced than simply lining up management expense ratios (MERs).

Several factors influence what you actually pay:

How your fees are charged

- Most mutual fund series embed advice and dealer compensation in the fund’s MER

- Some fee‑based accounts may use a lower‑MER fund, as they charge a separate advisory fee

- If you buy and sell investments on your own, you may also pay trading commissions or other transaction fees on each trade

What’s included in the fee

- Active strategies typically include the cost of professional management, research, trading, and risk oversight

- Passive strategies tend to have lower management costs, because the portfolio is built to follow an index, rather than relying on ongoing, research‑driven decisions from a manager

- Advisory fees cover financial planning, personalized recommendations, and ongoing support, and may be charged separately from the fund’s MER

That’s why it’s important to look at total cost in the context of total value, including the account structure, the type of strategy, and the advice and service you receive.

Everything you need in one portfolio?

At Scotiabank, active and passive aren’t opposing camps… they’re tools we can combine thoughtfully in our portfolio solutions. Because the aim isn’t to “win” the active vs passive debate, but to put both to work in a portfolio that fits you.

And with Scotia Essentials Portfolios, we blend actively managed mutual funds with cost‑effective index‑tracking ETFs, seeking the right mix of active insight and passive efficiency.