Our Rethinking series debunks common misconceptions about popular investing topics to help you stay informed. Today's topic: retirement. For many, retirement planning is often shaped by rules of thumb or commonly held beliefs. These assumptions can shape your retirement plan in ways you may not realize, quietly creating blind spots that often remain invisible until it’s too late to correct course. In this article, we explore three common retirement myths and highlight what to think about now to help keep your retirement plan on track.

Myth: Government pensions will cover all my retirement income needs

Picture this: you’re just a few short years away from retirement. As the countdown begins and retirement comes closer into view, you decide to crunch the numbers. When you factor in government benefits like the Canada Pension Plan (CPP)—or the Quebec Pension Plan (QPP) in Quebec—and Old Age Security (OAS), it can feel like you have a solid foundation. And you do —government benefits can play an important role in retirement income planning. But when those benefits are lined up against a long list of everyday expenses like groceries, utilities, property taxes, and the lifestyle choices that matter to you—such as travel or hobbies—it can become clear that government income may not cover everything you expect it to.

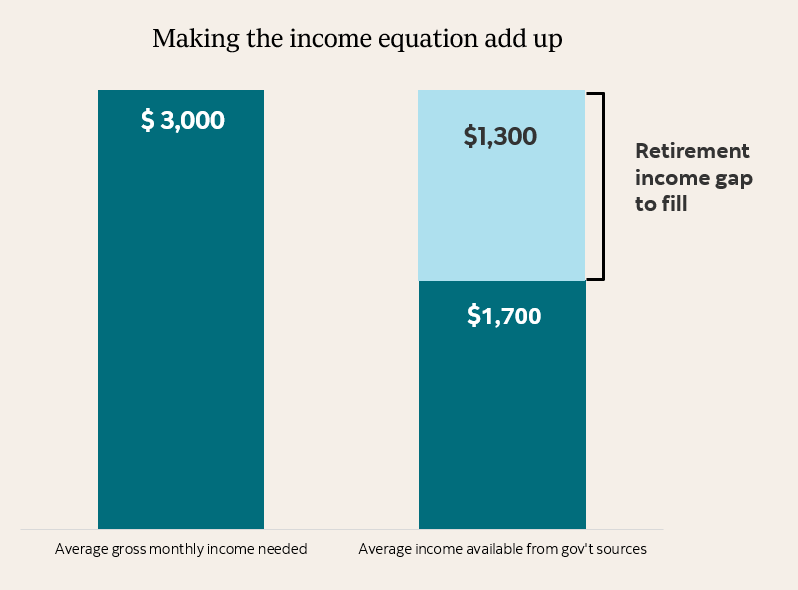

Here's the reality: government pensions were designed to replace part of your income—not all of it. That's where personal savings, investments, work pensions, and planning come in. In fact, that's exactly why the government created registered savings plans like the Registered Retirement Savings Plan (RRSP) and Tax Free Savings Account (TFSA)—to help and encourage Canadians to bridge the gap. To put this in perspective, Scotiabank research shows that among Canadians planning to withdraw a specific monthly amount in retirement, most (69%) expect to need $3,000 or more per month1. By comparison, even at today’s levels, CPP (about $950 per month)2 and OAS (about $750 per month)2 combined provide roughly $1,700 per month, leaving an income gap of around $1,300 that needs to be filled from other sources.

Figure 1: Mind the gap

The takeaway

Government pensions are designed to supplement your retirement income, not replace it entirely. By understanding how these government programs fit into your overall plan and supplementing them with other cash flow sources, you can build a retirement strategy that better supports your goals and lifestyle.

Myth: A paid‑off home means I’m set for retirement

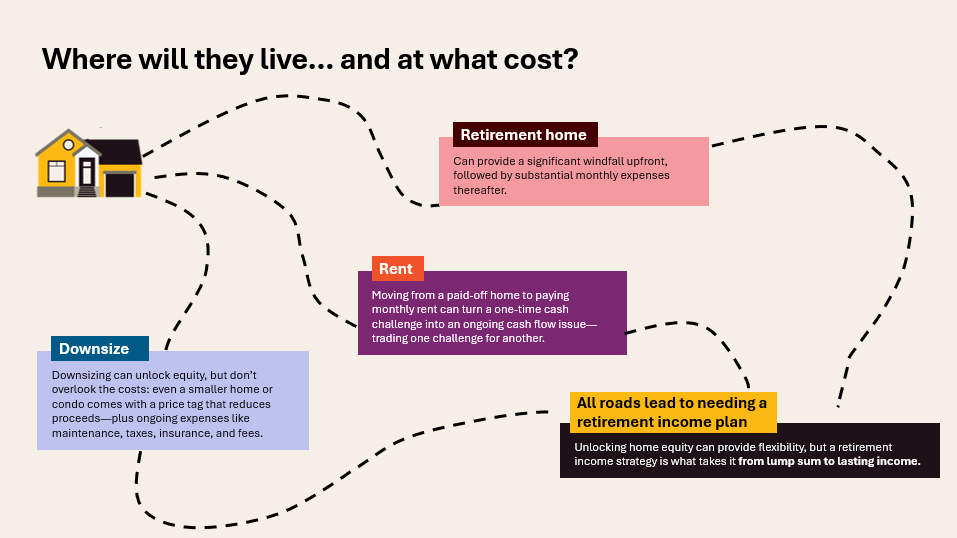

For many Canadians, their home is their most valuable asset. You can see it, you’ve invested in it, and it’s likely grown considerably in value over the years. So when you think about retirement, it’s natural to assume, “I’ll just sell my home and downsize or rent when the time comes.” A home as a retirement plan sounds solid – but is it?

Here are four things to consider:

The takeaway

Even if the sale of a home provides a sizable windfall, knowing how to turn that one-time lump sum into lasting retirement income is precisely why you need a retirement income plan, not a reason to go without one. So, while your home can be part of your retirement strategy— it works best as part of a broader plan that includes other cash flow sources designed to provide steady, reliable cash flow over time.

Myth: Now that I'm retired, I need to move my money to safer investments

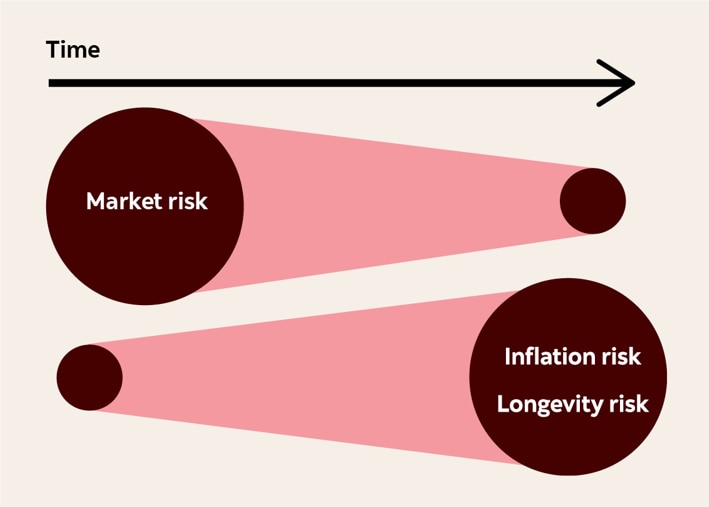

After years of saving for retirement, it's only natural to want to protect your nest egg. Lower-risk options like GICs might feel like a safe bet, but protection doesn't always mean preservation. Avoiding market risk entirely can introduce other risks that may be less obvious but can be just as important (see Figure 3). Inflation can erode your purchasing power over time, while longevity risk — the risk of outliving your savings — means your retirement could last longer than expected.

Figure 3: Safe today, short tomorrow?

After all, retirement isn't the end of the story—it's the start of a new chapter. And it's often a long one that can last 10, 20, or even 30+ years. So rather than asking "what's safest?" in retirement, the better question is "what's sustainable?". A balanced strategy that blends stability with growth potential can help your savings keep pace with inflation and sustain your cash flow for the long haul. Because preserving your money is good, but preserving your lifestyle is better.

The takeaway

Avoid trading one risk for another. A balanced approach can help protect not just your savings, but your quality of life throughout retirement. Scotia Essentials portfolios are designed with this balance in mind, helping investors stay invested with a mix of stability and growth.

The bottom line

What these myths reveal is a simple truth: retirement security doesn’t come from any single source or one‑size‑fits‑all formula. It comes from understanding the full picture — your cash flow sources, your assets, your timeline — and how they work together to sustain you through what may be decades in retirement.

Your advisor can help you map out your complete retirement picture, identify risks and opportunities that may otherwise be overlooked, and build a strategy tailored to your specific goals. Because the best time to strengthen your retirement plan isn't someday—it's now.

1 Source: Scotia Global Asset Management Investor Sentiment Survey (Fall 2025).

2 Source: Government of Canada, Canada Pension Plan (CPP) and Old Age Security (OAS) payment amounts; CPP reflects the average retirement benefit for new beneficiaries at age 65 (January 2026) and OAS reflects the maximum monthly pension for ages 65–74 (April to June 2026). All figures are rounded to the nearest $50.

3Source: Canadian Real Estate Association (CREA), National Aggregate Composite MLS® Home Price Index (HPI) benchmark prices, not seasonally adjusted, annual data (2022–2025).

Commissions, trailing commissions, management fees and expenses may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed their values change frequently, and past performance may not be repeated. This document has been prepared by Scotia Global Asset Management and is provided for information purposes only. Views expressed regarding a particular investment, economy, industry or market sector should not be considered an indication of trading intent of any of the mutual funds managed by Scotia Global Asset Management. These views are not to be relied upon as investment advice nor should they be considered a recommendation to buy or sell. These views are subject to change at any time based upon markets and other conditions, and we disclaim any responsibility to update such views. Information contained in this document, including information relating to interest rates, market conditions, tax rules, and other investment factors are subject to change without notice and Scotia Global Asset Management is not responsible to update this information. Nothing in this document is or should be relied upon as a promise or representation as to the future. To the extent this document contains information or data obtained from third party sources, it is believed to be accurate and reliable as of the date of publication, but Scotia Global Asset Management does not guarantee its accuracy or reliability.